Key Points:

• The software sector has underperformed the broad US market by around 35% since mid-2025.

• Some of this sell-off has been sparked by concern around the viability of SaaS business models in a world where anyone can build applications and software using AI. Despite having developed our own software using these tools, we think these fears are overblown. Much of the sector is a direct AI beneficiary even if the SaaS seat per model comes under strain.

• Additionally, hyperscalers have come under pressure given plans for enormous capex. This will be a key uncertainty overhanging the market for a while to come. The numbers are very large and it is not yet clear that the investment will be profitable.

• However, we still believe AI will generate strong productivity growth which should help the economy and non-tech corporates as a whole.

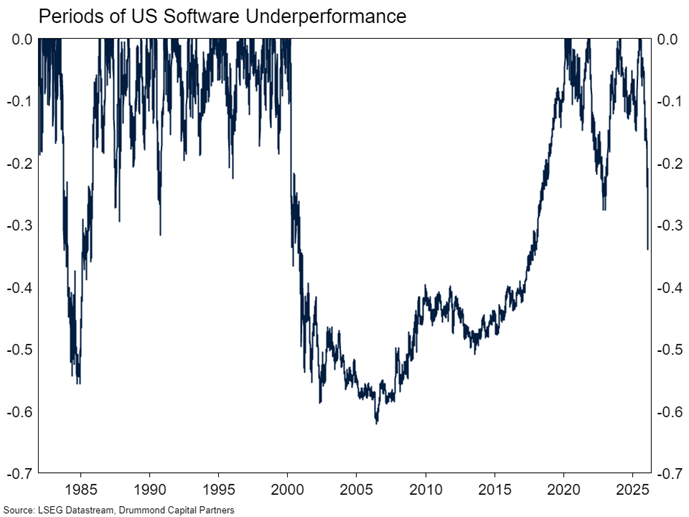

The software sector in the US is experiencing its most significant period of underperformance versus the S&P500 since the tech bubble. Since mid-last year, it has underperformed the broader US market by around 35%, with much of that underperformance occurring this calendar year. In this market insight, we review what’s going on under the hood of US equity markets and what’s driving the software sell-off.

SaaSpocalypse

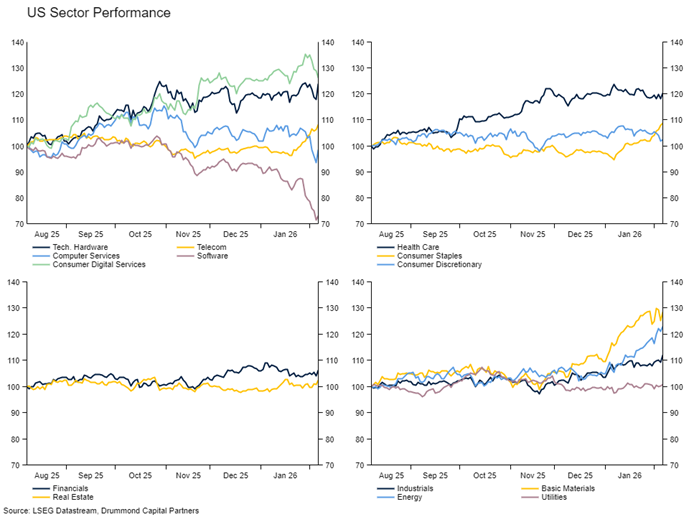

Before we begin, we need to put software in context of the broader market. The software sector is just over 9% of the total US market, and Microsoft is nearly half of that. That relatively small weight has been part of the reason why the overall index hasn’t been dragged down by software’s roughly 30% fall. The other reason is that some of the other sectors have been firing. Materials, energy, healthcare, consumer digital services (Google, Apple) and tech hardware (Nvidia) have risen more than 20% in the past six months. Staples and telecoms are up around 10% so far this year. Everything else has been doing relatively ok. It is a very software specific story.

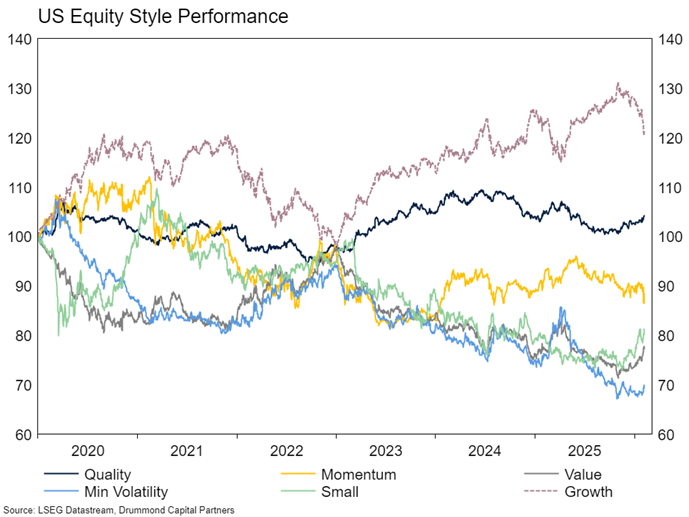

Weakness in software has coincided with some reasonable sector rotation within the US market. Growth as a style has underperformed the overall index by around 10% since late last year, though periods of reversion of a similar magnitude are common and the style has thus far avoided a more meaningful period of underperformance such as that in 2022. Quality as a style has started to outperform, which is somewhat unusual given the correlation between growth and quality we have seen for a number of years. Growth’s ugly, poor cousin, value, has of course outperformed during this period, as have small cap equities. Overall, the rotation we have seen isn’t really anything out of the ordinary, similar things happened in both 2025 and 2024. The key question of course is whether it continues.

The current market narrative is that the software sell-off was triggered by the release of Claude Cowork by Anthropic, a desktop application that gives non-technical users access to the agentic coding capabilities of Claude Code without having to use the terminal (PowerShell, Bash, CMD prompt, etc.). It’s a logical progression of the technology but initial users and reports, who perhaps haven’t been exposed to the functionality of Claude Code or Codex (OpenAI’s version) were surprised by the efficacy of the application, particularly the legal plug-in. We have been using Claude Code since the middle of last year and are more surprised by the market’s reaction than the technology.

The software panic thesis is as follows. Because individuals and corporations can build software internally easily using AI, SaaS as a business model is dead. Writing as someone who has used Claude Code to build software internally rather than outsourcing its creation, we think that logic only applies to a tiny fraction of the software sector. At an enterprise level, no one is rebuilding Windows to save a few hundred dollars a year. Indeed, if they wanted to save that money they could move their staff to Linux, a free operating system which has been available since the early 1990s. Open Office has been around since 2002 if you want a free version of Excel. There are companies at risk. Software providers that sell expensive software to large organisations (who have their own software development teams), which from a user’s perspective feels like trying to shove a square peg into a round hole, will now find it easier to build the square hole themselves. Start-up software companies will see the “value” of their technology stack dramatically reduced because the cost for the next start-up to replicate it is now much lower. We expect lots of innovation as the cost to develop software continues to collapse.

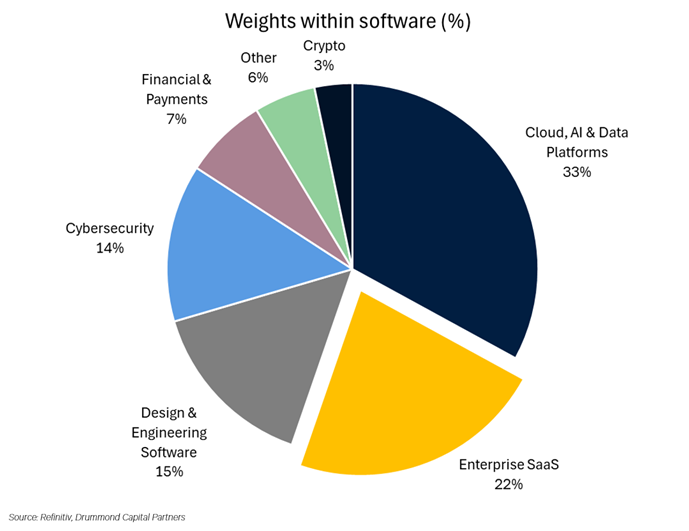

Alongside this, SaaS is only around one quarter of the software sector. Around 60% of the sector is cloud, data, cybersecurity and chip design software. Many of the companies in these categories are clear beneficiaries of AI. AI makes software development cheaper. Any good economist will tell you that supplying more of something makes it cheaper. Cheaper software means more software. More software means more databases, API calls, security checkpoints, compute requests, storage, chips, etc.

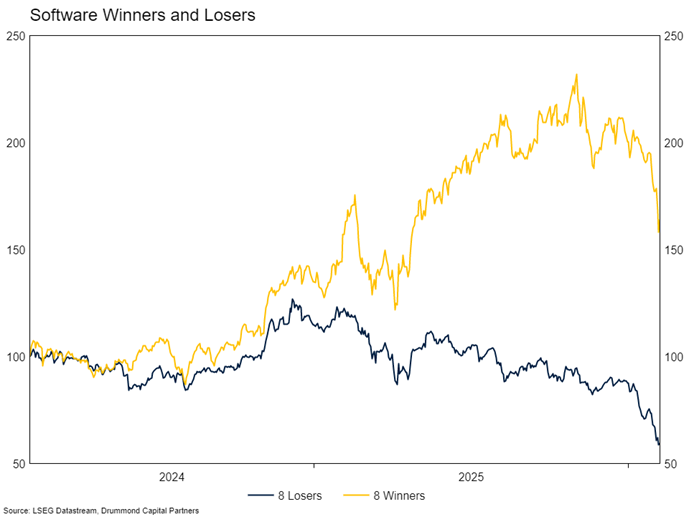

Given the above, we wonder if the market is throwing the baby out with the bathwater. We asked Claude to extract the winners and losers within the software sector based on their sensitivity to AI and SaaS disruption. The winners are names like Microsoft, Palantir, Synopsys and CrowdStrike. Companies that either sell the AI infrastructure itself, design the chips that power it, or provide the required security. The losers are the traditional SaaS vendors. Salesforce, ServiceNow, Adobe, Workday and others, whose per-seat subscription models are most vulnerable as AI coding agents increasingly allow enterprises to build internally what they previously rented. The winners were clear winners until late last year, outperforming the losers by more than 100%. However, the recent sell-off has taken the winners down by around 30%. Most of these names trade at extremely optimistic valuation multiples, so perhaps a correction is justified based on that. We don’t think it was justified based on Claude.

The Actual Elephant

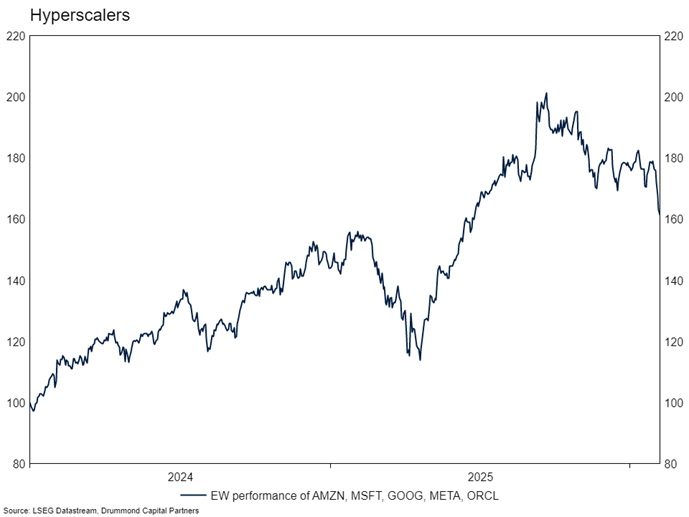

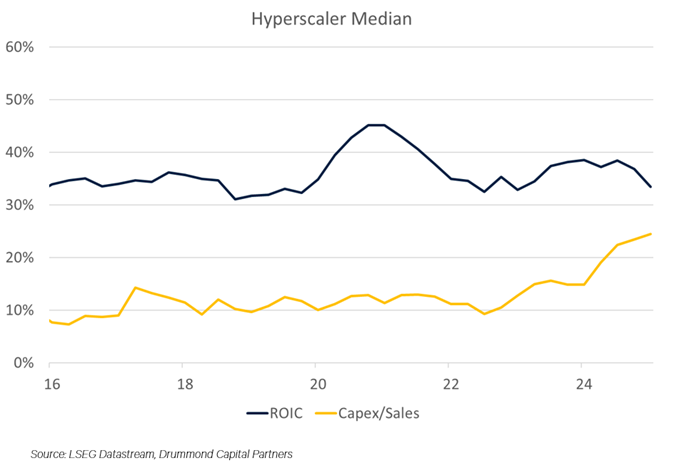

The other technology related drawdown making headlines is the fall in the hyperscalers. An equal- weighted basket of Amazon, Microsoft (which is in the software sector above), Meta, Alphabet and Oracle is down around 20% since September. The market is concerned that these companies are taking the hyper in their hyperscaler too literally with regards to capex.

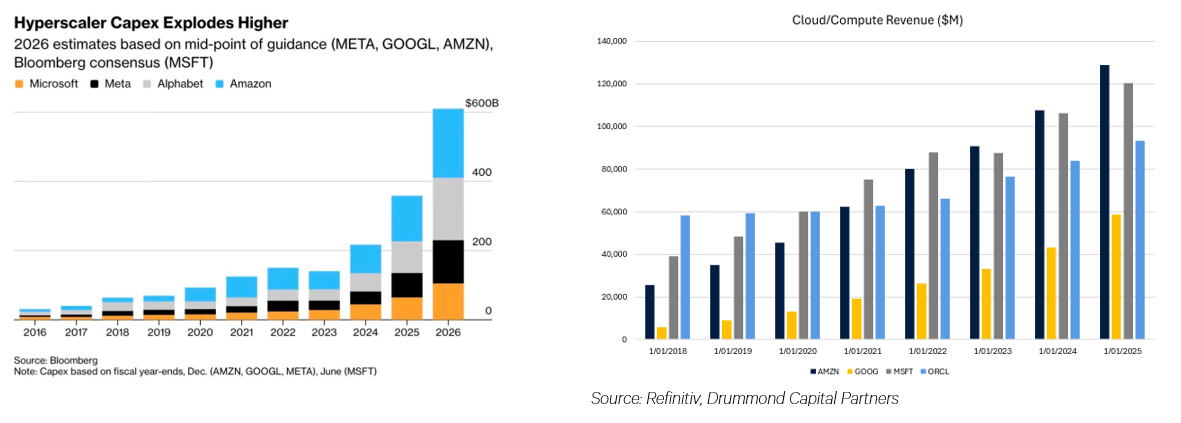

They may be correct, they may be incorrect. It’s probably the biggest question overhanging markets and may remain unresolved for years. We know two things. Proposed capex is extremely high, planned at ~$600 billion this year, three times higher than 2024. It may go higher from there. Additionally, the revenue these companies have been generating from selling cloud computing has also been rising at an exceptional pace. Meta is excluded. They are a hyperscaler which doesn’t sell their compute. More AI and more software means more compute is needed. Almost certainly cloud computing revenue will continue to rise, but whether the whole exercise will be profitable remains to be seen. Historically, companies have tended to overinvest in production in boom time environments, oversupplying the market and causing an inevitable downturn. Perhaps AI is different.

At the moment, the capex splurge hasn’t meaningfully impacted the profitability of the hyperscalers. Spending in the aggregate has been funded internally, meaning balance sheets aren’t under strain. Though debt issuance from the hyperscalers is likely to become more common, a big change from companies that grew from revenue.

The Singularity

We first wrote about AI nearly three years ago. Back then we believed AI would boost economy-wide productivity. We wrote:

The practical application of this technology, even as it is available now, is meaningful. A teacher could prompt an AI to generate ideas for lesson plans. Doctors could seek AI input into diagnosis, prompting with medical history, test results and current symptoms. Lawyers could ask AI to summarise all historical precedent related to a specific topic. Developers can use AI to help write code – this is a big one and the improvements here will be enormous. Marketers can ask AI to help generate potential campaign images and videos. There are real practical applications from this technology now and we imagine the workplace enhancements in one, three or ten years time will be manifestly greater still.

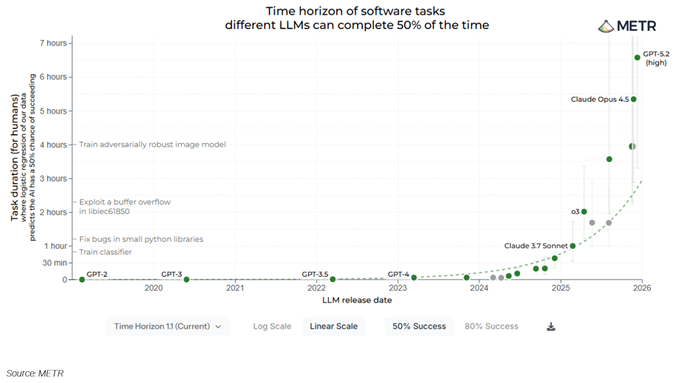

In the past three years the ability of AI to do those things in a user friendly, close to error-free, way has exceeded expectations. It has gone from a novelty to something that touches many people’s lives regularly. The hyperscalers are planning to deploy nearly as much compute capacity into the market this year as they did in the three years since we first wrote about AI.

No one knows how any of this will play out. We think AI will be the most disruptive technology since electricity. There will be winners and losers, but it should be disruptive in a positive way for the economy and markets overall. A positive productivity supply side shock should lift most boats. The capability of AI is still rising at an exponential rate. Unless AI creates the singularity, that will tail off at some point. Regardless, deployment into the real economy by corporates lags the forefront of model capability so much that even with no progress on actual AI, the benefits will still flow for years to come.

Portfolio Positioning

Our portfolios are currently long growth exposure, but within equities we have a strong bias towards diversification across region and style. We love AI, but so does everyone else and until recently that was very much in the price. Meanwhile, much better value can be found across regular listed companies who are yet to reap the benefit of AI adoption in their day-to-day operations. Perhaps this technology software and hyperscaler sell-off will continue, providing an attractive entry point to pivot back towards a growth and technology bias, but it is too soon to tell.

Prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only.

The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatements of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance.

This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that it is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.

-p-500.png)