Key Points:

· Next year could be another relatively benign year for global markets. Recession risks are low and the earnings outlook is solid.

· We could see a broadening in market returns away from big tech priced to perfection towards other sectors which have better valuations or could be the beneficiaries of AI application rather than infrastructure provision.

· As always there are risks to this outlook. We think the return of a rate hiking cycle would be a headwind to markets. China’s economic growth is again slowing and Trump remains a wildcard.

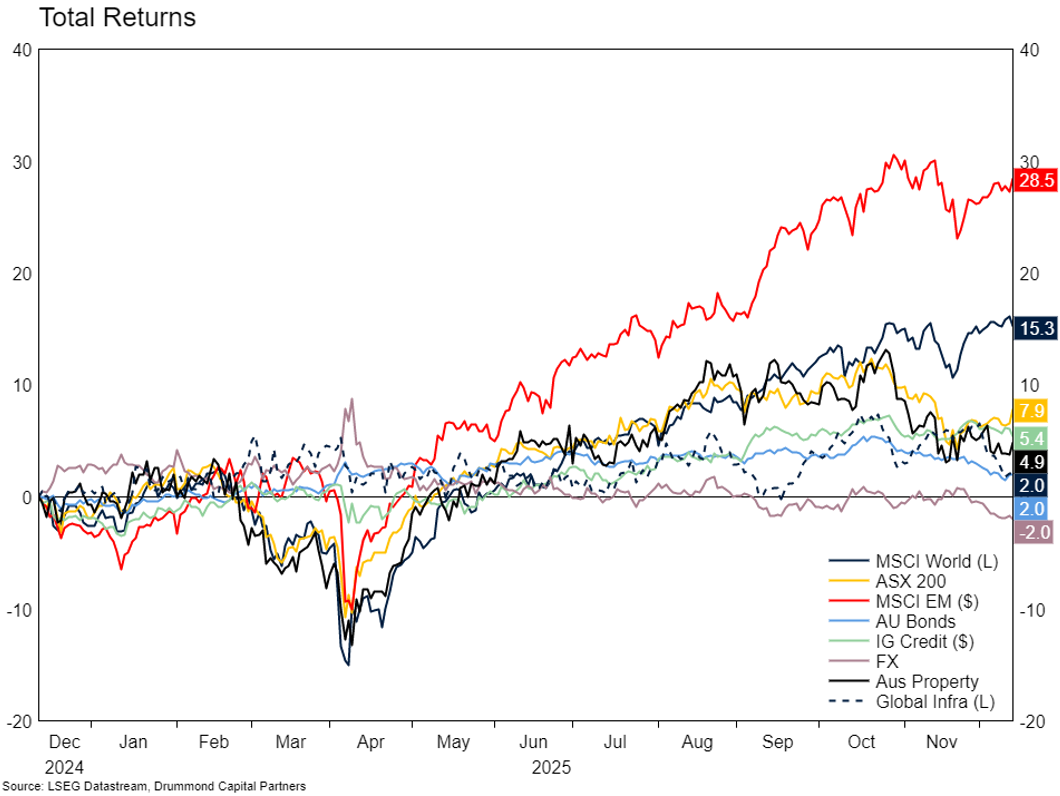

Once again, it’s that magical time of the year where we write an outlook for the year ahead. The end of the year provides an opportunity to spend time with family and friends reviewing how accurate last year’s outlook was and to (hopefully) be thankful for the investment returns markets have delivered. This time last year, we wrote that 2025 was shaping up to be “normal”. In retrospect, that turned out to be the case, though with a substantial wobble in the second quarter of 2025. We thought there would be some interest rate cuts globally (there was) and some potential for market rotation (value, emerging markets (EM), Europe and Asia all did well, though small and mid-cap equities still struggled). One of the key risks we outlined, White House chaos, certainly proved to move markets (albeit not for long). None of the others eventuated. All in all, a pretty good year which delivered ~15% returns from global equity markets and around long-term average returns from Australian equities.

The Year Ahead

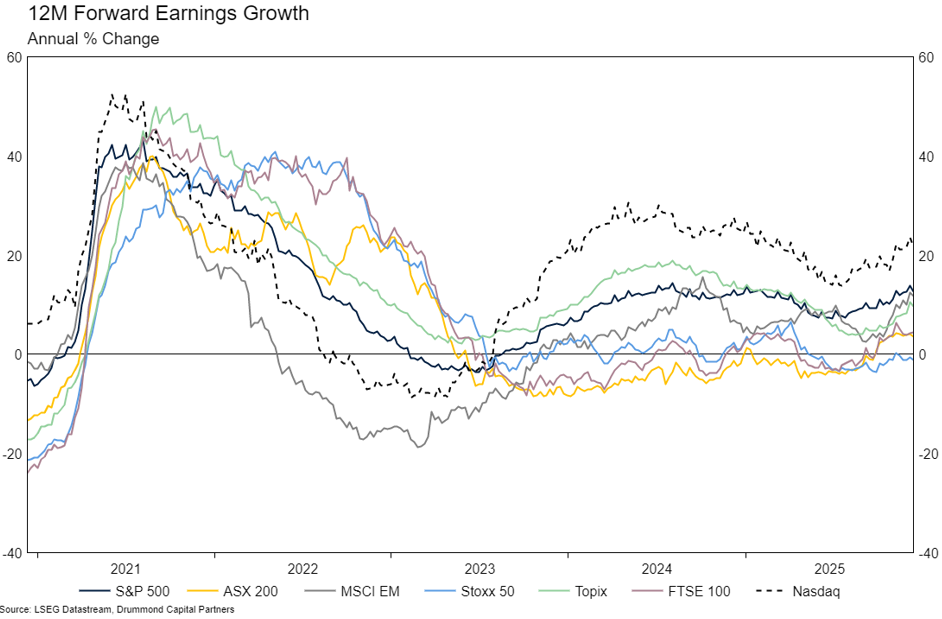

Will 2026 be a repeat? Our central case for markets and the global economy remains relatively benign, though as always there are risks hanging over us. The widespread interest rate cuts over the past couple of years have put a floor under economic growth for major developed market economies and as a result, the risk of recession (which still lingered last year, especially with the Sahm rule being triggered) has been finally put to bed. We tend to not place too much weight on consensus economic forecasts, but for what they are worth they are suggesting global economic growth around the long run average in 2026. This benign outlook has translated into relatively solid earnings growth expectations, with the usual suspects (US tech sector) leading the pack in terms of optimism.

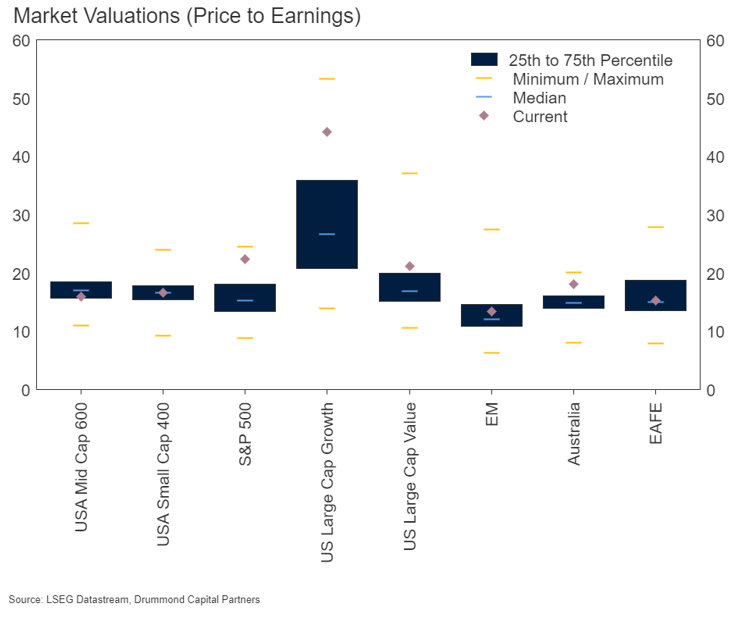

For the US equity market, strong expected earnings growth comes with very high valuations. As has been the unusual case for a couple of years, Australian equity valuations are also very high, despite very little expected earnings growth. Elsewhere, valuations are largely normal, including for the US small and mid-cap sectors.

What the net of the above means for returns next year is debatable. If US tech companies continue to deliver exceptional earnings growth, investors will continue to be happy to keep their valuations lofty and they can again outperform the market on average. However, high expectations are by definition hard to beat and we have seen some market wobbles this year on tech worries. We think next year will not be easier on that front. Otherwise, in an environment of reasonable global economic growth, perhaps rotation can continue and previously unloved parts of the market can benefit from multiple expansion and reasonable earnings growth. With no clear answer, like in 2025 we think holding a bit of everything is a good baseline strategy from an equities portfolio construction perspective.

REITs and infrastructure have benefited from tailwinds in the form of lower interest rates and global data centre buildouts, but have struggled with high replacement/improvement costs for legacy assets, a slow return to the office and the politicisation of energy policy in most economies. We think little of this will change next year, though perhaps tailwinds from falling interest rates will fade.

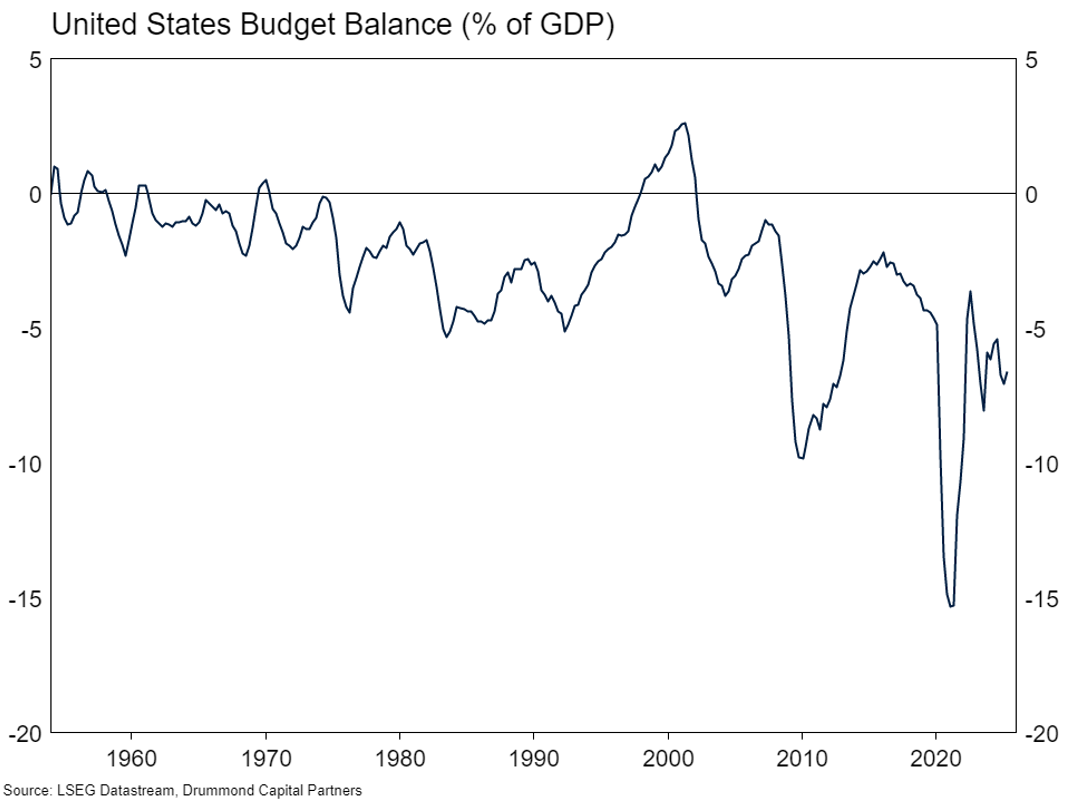

Within defensive assets the key question will be how long investors will be happy to fund governments with terrible fiscal trajectories, particularly the US Government, at rates not that far above inflation. For now at least, it doesn’t seem like the credibility of government debt is being called into question and long-term rates in the US and Australia will average around 4.5% with a bit of fluctuation. With credit spreads very tight, there are few prospects for outsized returns in this asset class, though it still appears attractive from a risk/reward perspective relative to government bonds.

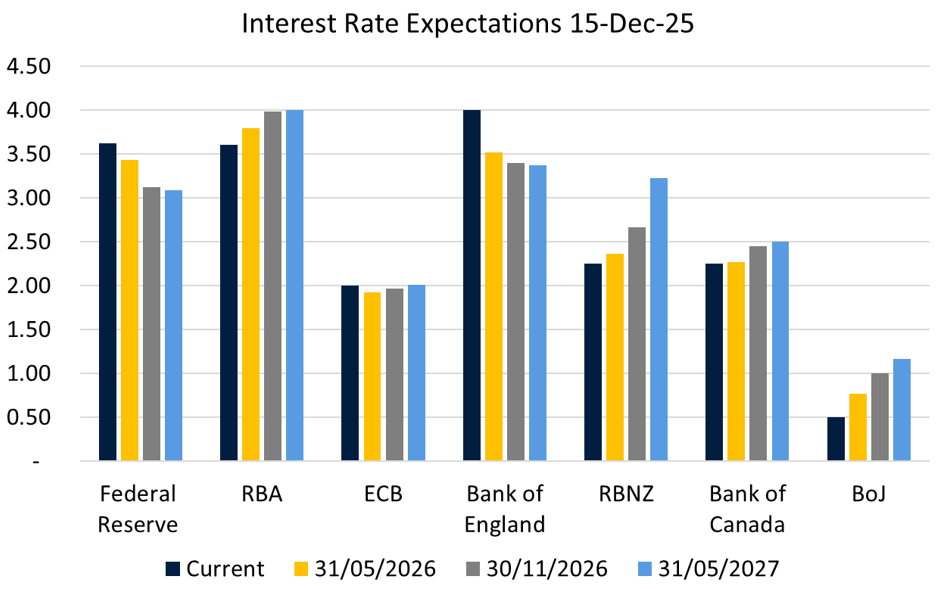

Perhaps where 2026 will differ from 2025 will be a divergence in the interest rate outlook across economies. Aside from Japan, 2025 followed 2024 as a year of widespread interest rate cuts. However, 2026 is shaping up to be a year of divergence. The US Federal Reserve and Bank of England are still expected to cut rates a little more next year, but the European Central Bank is now on hold and the RBA, Bank of Canada and RBNZ have all switched to hiking mode. We would not be surprised at all if this time next year the market expects next Federal Reserve move to be a hike rather than a cut. The transition towards a global hiking cycle from a cutting cycle would represent a headwind to global equity and bond markets, though this is by no means certain and isn’t likely to be part of the market narrative until late next year (if at all).

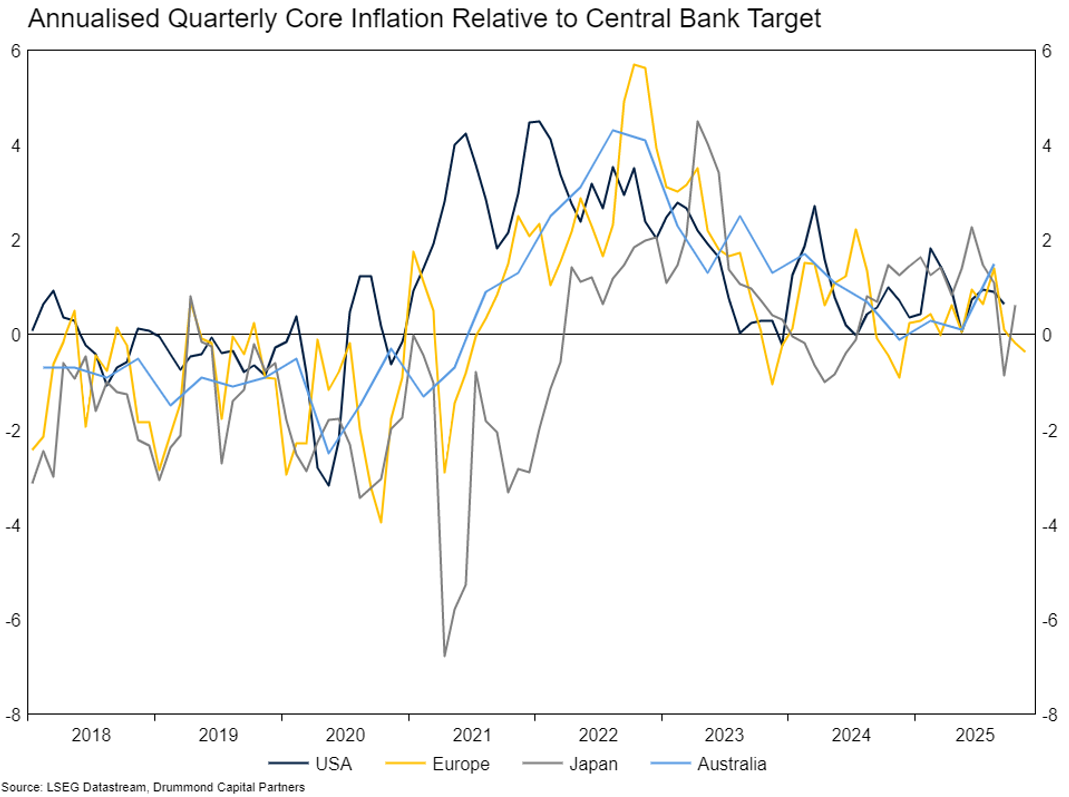

The risk here is inflation. Despite still too high inflation, concern about tariffs and labour market weakness has kept monetary policy expectations firmly in the easing category in the US. However, inflation in many major economies remains uncomfortably a little bit above target. If growth strengthens in the US and elsewhere, there is a reasonable chance a hiking cycle becomes forefront in the market narrative earlier than expected.

Key 2026 Themes and Risks

With the backdrop to 2026 relatively positive, there are a few other key themes which we think can influence markets alongside the baseline narrative.

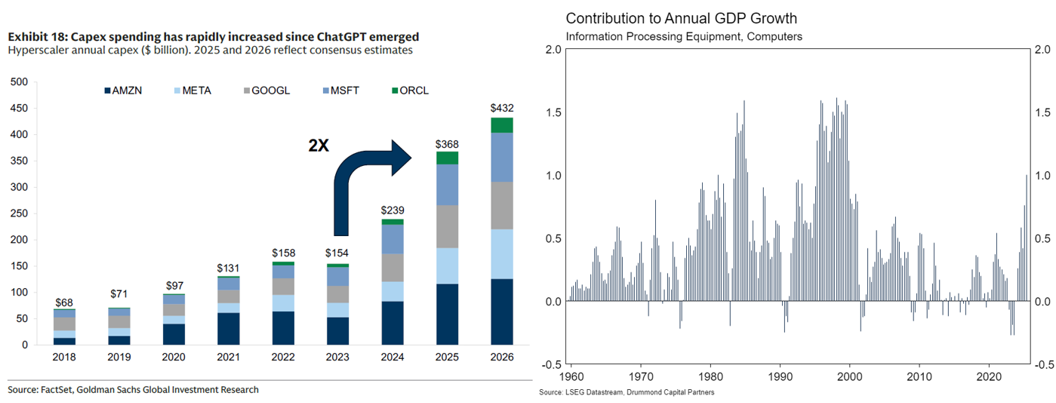

The first major consideration is the outlook for the tech sector in the US. This sector has been a key driver of global markets for a number of years and next year will be no exception. We are still quite positive on AI as a thematic. We use it every day and the productivity enhancement it has driven in our business is meaningful. It is also clear that investment in AI is helping to support overall economic growth in the US and elsewhere. The capital expenditure is huge, and if the 1990s personal computer revolution is any proxy, could continue for many years in the future.

However, whether there will be sufficient return on investment for the companies investing in the technology is unclear. Capex as a share of sales has more than doubled for hyper scalers, though this has not yet been felt in terms of lower ROIC. Revenue projections for AI companies seem high, but not unreasonable given the likelihood they will touch most people’s lives on a daily basis. We think the balance of who wins AI (the infrastructure providers or main street businesses) is much more relevant for sectors within the equity market (value versus growth, technology versus industrials) than the equity market as a whole. Again, owning the whole market in a diversified fashion is probably the surest and safest way to capture continued AI upside.

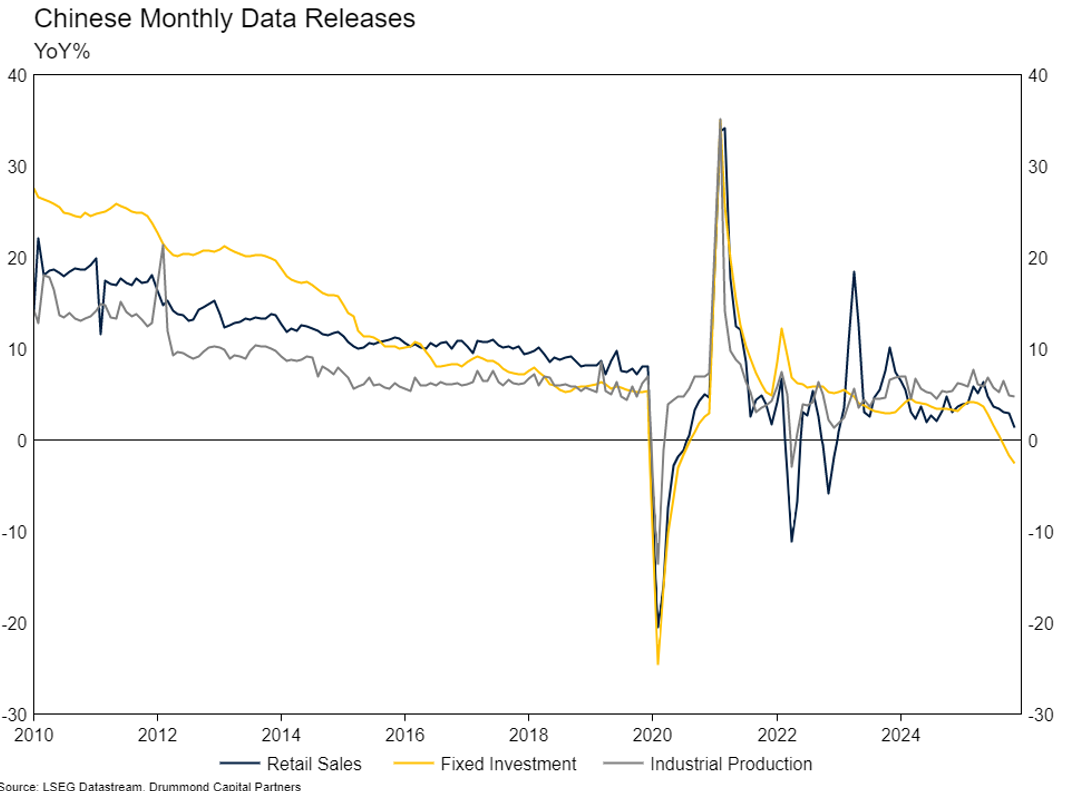

Renewed China weakness is another major thematic we think will impact markets next year. After what looked like a period of consolidation following government stimulus and interest rate cuts, the housing market in China is again weakening and again taking consumer and business confidence down with it. Previously, the contracting housing market had been in part offset by massive investment in manufacturing capacity across secularly important sectors (solar, battery, EVs, chips, defence). However, particularly with respect to the first three, vast investment in capacity has exceeded the rest of the world’s ability to absorb the production. There is no one left to buy additional solar panels and EVs at a price that is economical for China’s producers. So far, the market has been looking beyond this. This is in large part because of positivity around China’s tech sector, which has done an amazing job of keeping up with the US despite high technology export controls and remains quite attractively valued versus its US counterpart. At some point, attention will turn back to the real economy, and the Government will again need to act to prevent recession.

The last thematic is the bane of investment strategists around the world – Trump. The whip saw in markets we saw in April this year around tariff announcements shows the damage that can be done by poorly planned and terribly implemented economic policy in the world’s large stand most important economy. Our expectation is that Trump will continue to throw wildcards at markets, but there is nuance to the timelines here. A key short-term milestone will be the US Supreme Court’s ruling on the legality of Trump’s tariff policies. Should, as expected, the Court rule the tariffs illegal there are a few potential pathways forward. We would expect a raft of new tariffs under different authority/statutes to attempt to replicate the existing mix. If the Court demands tariffs be refunded, it will represent a relatively substantial short term fiscal injection into the US economy. There is also the risk that the Trump administration ignores the Supreme Court, though that would represent a material deterioration of the rule of law and democracy in the USA.

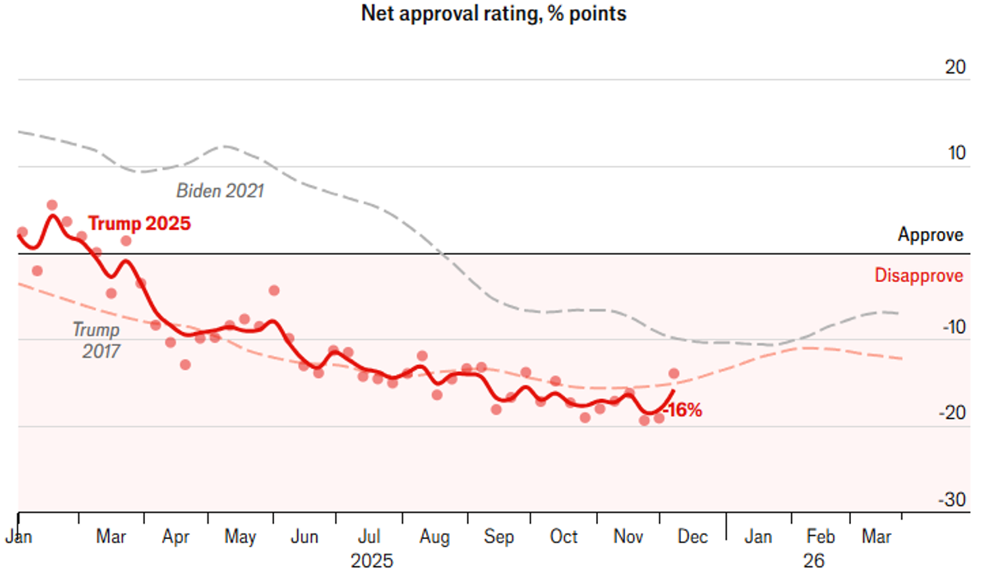

Beyond the tariff ruling, a more significant milestone will be the US mid-terms, scheduled for November 2026. We expect that between now and then, Trump will do everything in his power to undermine democratic process to attempt Republican control of both Houses of Congress. Still, power is currently held by a narrow margin and Trump’s approval rating is much lower than when he was elected, suggesting the Republicans will lose control of the Senate and potentially the House of Representatives. A divided Congress will take much of the “Trump risk” away, we just need to maintain the rule of law and democracy until then. In between these two dates, it is almost certain that Trump will nominate an uber-dove to lead the Federal Reserve when Chairman Powell’s term ends in May 2026. This could spark some weakness in the long end of the bond yield curve, but is also growth positive, which should support equity markets.

Portfolio Positioning

In line with a relatively benign outlook, our portfolios are modestly overweight growth exposure, with a tilt towards global equities away from Australian equities. Within global equities we have a quite diversified mix across style and region, with explicit exposures to Asia and global small caps. We are also underweight government bonds versus credit in line with the views above.

Prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only.

The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatements of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance.

This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that it is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.

-p-500.png)