Key Points:

• The Australian economy has been soggy for a number of years, reflecting (we think) excess government spending and regulation, weak productivity growth and an over-reliance on the property market.

• However, with interest rates coming down a bit, there is some room for household spending to improve, which could drive a recovery in business confidence and investment.

• This positivity has translated into an improvement in earnings expectations for the ASX 200, but with valuations exceptional, this hasn’t translated into market outperformance. We think we would need evidence of more rate cuts and an enduring economic recovery for that to be the case.

It has been a little while since we wrote about Australia. Long time readers of this note will struggle to recall a time where we have been positive on the Australian economy or equity market. In this month’s Market Insight, we rehash the outlook for Australia, seeing if there has been any improvement and where the risks lay.

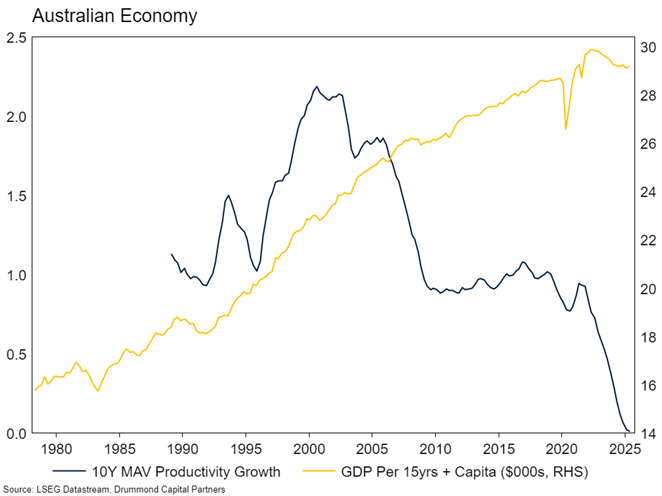

It has been a rough few years for the Australian economy. On a per person basis, the economy has been shrinking since mid-2022. Productivity growth has collapsed to zero. Real wages (adjusting for inflation) are well below where they were in 2020. We spent a bit of time outlining what we thought were the primary causes of this weakness in our December 2024 Insight, Down Under & Out. The key failing of the economy has been no productivity growth. We think has been caused by public sector spending crowding out the private sector, a regulatory burden which is too high and a disproportionate focus on the housing market as a store of household wealth, leading to elevated household debt levels.

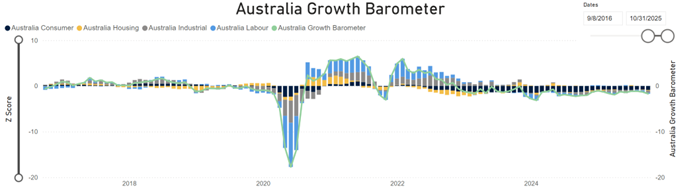

The malaise is also shown by our Growth Barometer, which shows an economy holding its head just below the water line for a number of years, dragged down by a weak consumer (dark blue bar).

What would it take for the economy to begin to grow again? In our view, it is not impossible, but the path for a sustainable return to growth is relatively narrow. We are assuming here that the Government side of the equation is largely fixed. It seems very unlikely that any Australian government has the appetite for a meaningful pro-growth economic reform or deregulatory agenda.

The biggest problems with the economy tend to benefit powerful electoral cohorts and lobby groups. Part of the reason the NDIS has become untouchable despite its ballooning costs is because it's the country's largest employment program. Infrastructure costs continue to explode higher because tier-1 construction workers command packages that would make tech workers blush. Housing unaffordability suits the two-thirds of voters who already own property. Even our tax system, which everyone agrees needs reform, remains frozen because any meaningful change would require changes to much loved tax concessions.

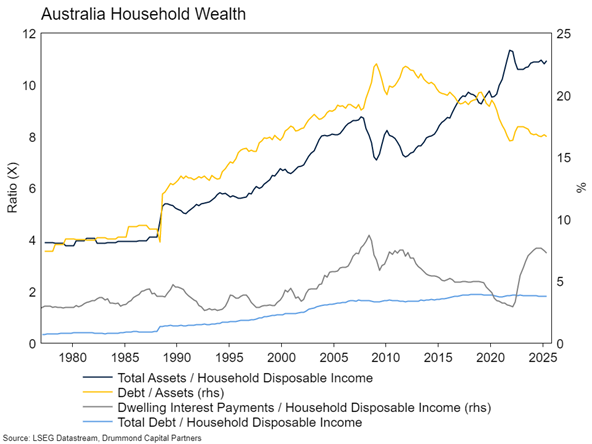

So, failing a change in the rules of the game, what could drive growth? The most likely trigger is an improvement in household spending. Though wages and employment growth are weak, some households in Australia have ample capacity to increase spending. Economy wide, the net asset position of households is staggeringly large. Net assets are around nine times total disposable household income. Most of this is housing, but a surprisingly significant proportion is in financial assets (largely superannuation). Households are generally less predisposed to spend increases in wealth than income, but the capacity is there. Of course, for housing wealth accessing this capacity requires higher levels of gearing. And that’s the counterpoint to the “Australians are wealthy” argument. Although we are asset rich, those asset values are held up by a heroic amount of household debt.

These high levels of household debt are certainly a challenge to the “wealth sparks a consumer recovery” hope. However, if you again look to the chart above, you will note that the grey line is around historic highs. Mortgage interest payments as a share of income remain very high, despite the beginning of the RBA’s rate cutting cycle. However, the RBA has ample capacity to cut rates further, which could support household spending meaningfully.

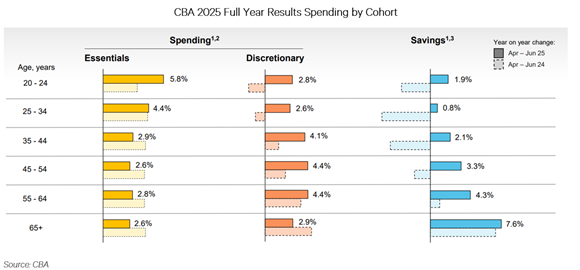

Indeed, we can see some evidence of this, alongside some interesting nuance, in the chart below, which shows spending patterns in the CBA customer base broken down by age cohort. A year ago, it was clear that younger households were suffering the most from high interest rates (and rents). Their discretionary spending was falling, and they were tapping into savings to make ends meet. Last year’s version of that chart also showed that spending and saving in older age cohorts had risen over the period relative to a year earlier. That makes sense. They own investment properties and term deposits, normally having no debt and hence benefit from higher interest rates. Now, we can see that spending patterns have normalised, with younger cohorts beginning to spend and save again.

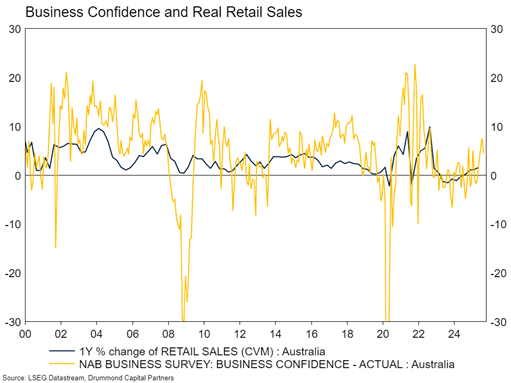

Confidence around lower interest rates and some recovery in consumer spending has boosted business confidence, which is now closer to long run average. A recovery in business confidence could translate into stronger growth in business investment. Reported capex intentions overall have begun to rise, driven by an improvement in expectations for the non-mining sector. Domestic data centre investment is also boosting overall business investment. There is significant room for improvement here. More capex could also boost productivity growth – a lack of capital deepening has been flagged by the RBA as part of the reason for poor productivity growth.

Lower interest rates should also support residential construction, which despite record high house prices and very strong immigration-induced demand, remains around 10% lower than in 2018. Basically, lower interest rates are working as they should. Borrowing costs across the economy have fallen and that is supporting economic activity, even with the overhang of government and regulation slowing things down.

What could derail the green shoots of recovery? At the moment, markets are pricing only around a bit more than one rate cut from the RBA. That may not be enough to really get the economy back into gear. The reason for rate cut hesitation is reasonable. Like most major economies, the last stretch of inflation normalisation has been tough to reduce.

The other area of potential risk is around a bad credit cycle / rising unemployment rate. Whilst consumer bad debts have risen modestly, business insolvencies have risen substantially and are approaching post Financial Crisis rates. Should this continue and translate into higher unemployment rates (given employment growth is already slowing down) this could stifle any positivity around the overall economy.

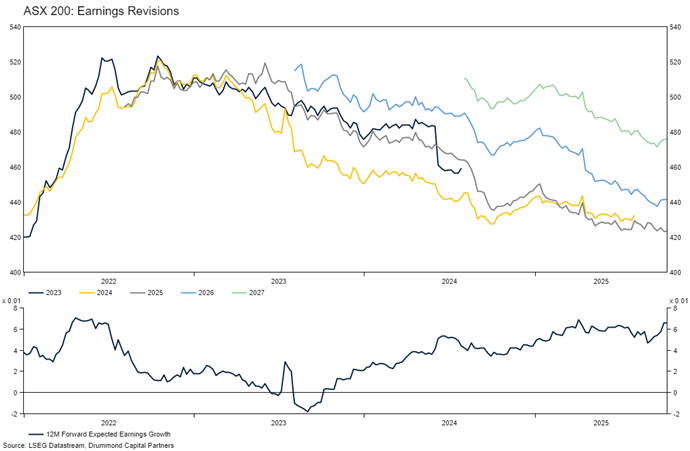

Green shoots around the economy have driven an improvement in earnings expectations for the ASX 200 (see below). However, the market still isn’t outperforming global equities, likely reflecting very high valuations (which need solid earnings growth to be justified) and the lack of a meaningful technology sector.

Portfolio Considerations

Our portfolios are currently slightly underweight Australian equities. Although there are some green shoots in the economy, the starting point is pretty sanguine and valuations are exceptional – the ASX is on a similar forward PE multiple to Google. That said, if inflation moderates a bit giving the RBA capacity for more rate cuts than are currently priced, there would be more capacity for a more meaningful recovery in growth and potentially a larger allocation to the asset class.

Prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only.

The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatements of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance.

This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that it is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.

-p-500.png)