Key Points:

· More than a decade since Abenomics was launched, a reform agenda in Japan is bearing fruit.

· While there hasn’t been a meaningful acceleration in economic growth, deflation looks to have been defeated and there has been substantial corporate governance reform, aiming to lift corporate profitability and shareholder returns.

· If anything, the corporate governance reform agenda has accelerated in recent years, which, combined with comparatively cheap valuations for the Japanese equity market suggests there is scope for solid relative returns from here.

Japan is not a country that many Australians have had much equity exposure to historically. Fighting the hangover of the 80’s equity market heyday and structural growth detractors of an aging population and deflation, it has been an equity market that was easy to ignore. That is despite Japan being 3 times the size of Australia within global equity benchmarks. In this month’s Market Insight, we dive deeper into the Japanese economy and equity market. With more than a decade having passed since the launch of “Abenomics,” how much has changed for the Japanese economy? The short answer is a lot. The long answer is below.

A Reform Journey

Abenomics was introduced by Prime Minister Shinzo Abe in 2012 and was an economic revival strategy designed to end Japan's two-decade deflationary spiral through "three arrows" of coordinated policy intervention. The first arrow involved aggressive monetary easing by the Bank of Japan, including negative interest rates and massive asset purchases. The second arrow deployed fiscal stimulus through increased government spending on infrastructure. The third arrow promised structural reforms to boost productivity and competitiveness, including labour market liberalisation, corporate tax cuts and corporate governance reform. Abe resigned as Prime Minister in 2020 and has been succeeded by a number of leaders of varying degrees of market friendliness. However, the October 2025 appointment of Sanae Takaichi (an Abe protégé) as Prime Minister (albeit leading a minority government) has reignited investor hopes for Japanese equities.

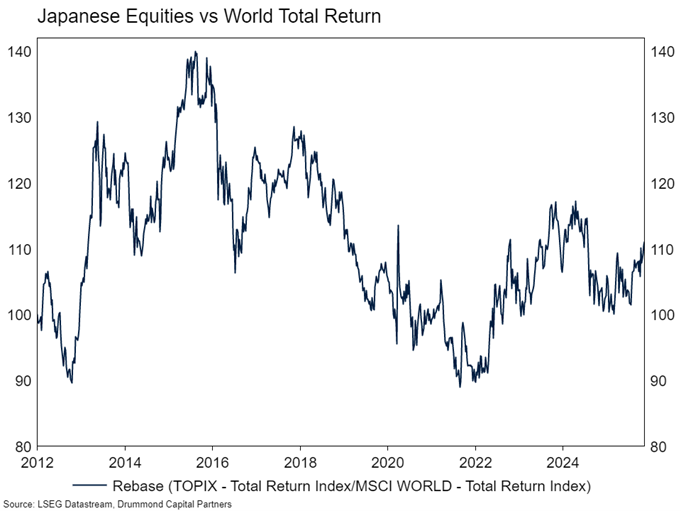

Abe’s reform agenda sparked a relatively spectacular three-year period of outperformance in Japanese equities versus the rest of the world in local currency terms. However, from 2016 to 2022, all of this outperformance was given back as the market failed to keep up with US mega cap technology companies. Since 2022, the Japanese equity market has been outperforming again. Much of this performance has been influenced by currency moves. A falling Yen, which was a key element of the three arrows agenda, has traditionally boosted Japanese equities in local currency terms as exporters become more globally competitive.

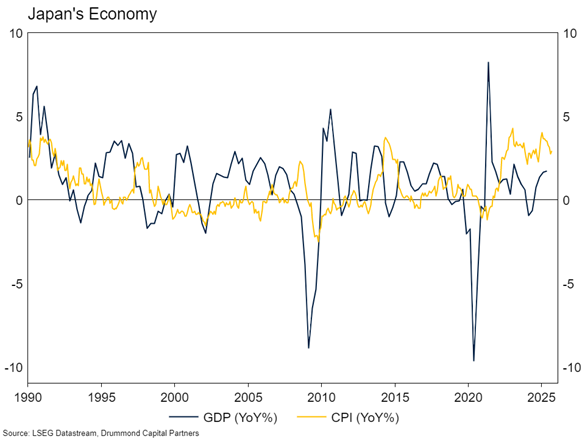

What about the economy? Did the reform agenda have much of an impact? On the economic growth front, it is hard to discern a material change. Real economic growth remains volatile, at rates around where it has historically trended. Reported labour productivity doesn’t look to have accelerated materially. However, it seems clear that Japan’s period of deflation is now over. Headline inflation has remained above the Bank of Japan’s target for a number of years now, initially kicked higher by the global inflation acceleration following Covid stimulus and the Ukraine war in 2021. While inflation in most other economies has returned close to target (though remains a little high), Japan’s inflation seems more persistent. The Bank of Japan was late to the rate hike party versus other central banks. Likely in response to the long legacy of deflation, the main policy rate in Japan was below zero until March 2024 and is currently sitting only at 0.5%. The Federal Reserve had finished its hiking cycle by then, having increased interest rates by more than 5 percentage points over 2022 and 2023. With inflation still high, the Bank of Japan is expected to continue to increase interest rates over the year ahead, in contrast to most other major central banks which are either on hold or cutting.

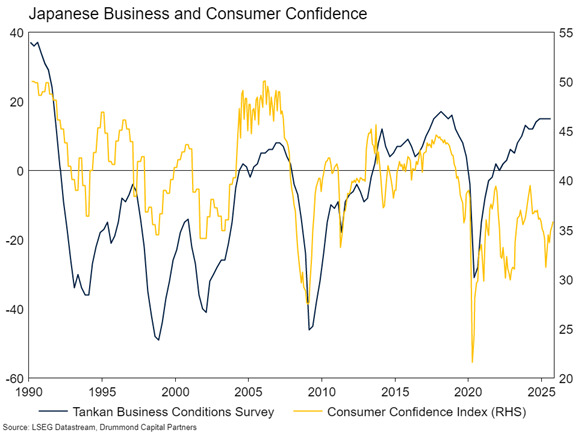

High inflation and rising interest rates have weighed on Japanese consumer confidence (see below). However, a weaker Yen and an inflationary environment have delivered pricing power to Japanese corporates. This, combined with the ongoing reform agenda has seen business confidence return to multi-decade highs.

But the economy is not the market, and the main positive story around Japan’s equity market reflects the intersection of corporate governance reform and cheap valuations.

Corporate Reform

Since Abe was elected in late 2012, there has been a concerted effort by Japanese authorities to improve governance within the corporate sector. This has been in the form of sweeping governance reforms to modernise corporate practices and improve shareholder returns. The Tokyo Stock Exchange (TSE)restructured its rules in 2022, creating stricter listing standards for its premium "Prime" segment, including requirements that at least one-third of directors to be independent and financial disclosures be in English. Most notably, in March 2023, the TSE began requiring companies trading below book value to submit and disclose concrete plans for improving their return on equity and capital efficiency. Companies that fail to comply face potential delisting from major indices by 2028.

The Financial Services Agency has updated both the Stewardship Code and Corporate Governance Code to strengthen investor rights and board accountability. New rules target cross-shareholdings—where companies hold each other's shares for relationship purposes rather than investment returns—requiring detailed disclosure when these positions are sold or reclassified. The FSA has also introduced stricter requirements for board independence, with recommendations for majority-independent boards for globally competitive companies, and mandated disclosure of board skills matrices and diversity metrics including gender and nationality targets.

Starting in 2027, large companies will face mandatory sustainability reporting requirements based on Japanese standards aligned with international frameworks. The reforms extend to executive compensation, requiring disclosure of performance-based pay structures and human capital strategies. These changes mark a fundamental shift from Japan's traditional stakeholder model toward explicit prioritisation of shareholder value, with regulators using both carrots (prestigious index inclusion) and sticks (delisting threats) to drive compliance. The TSE publishes monthly lists of compliant companies, creating public pressure on laggards to accelerate their governance improvements.

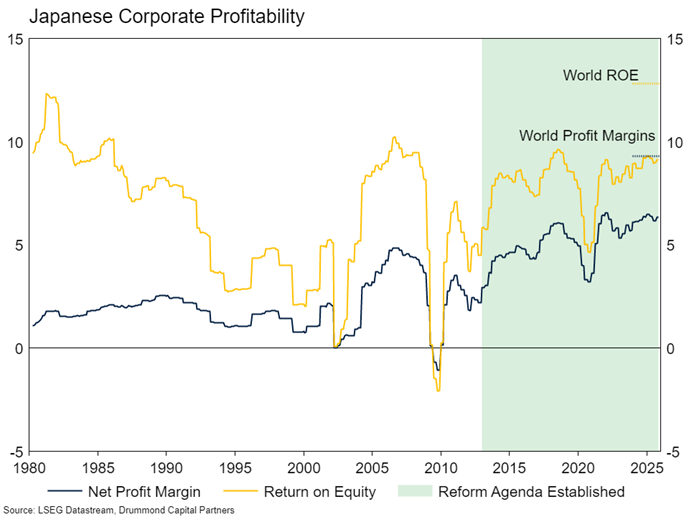

While the initial boost to markets from monetary easing and stimulus have faded since 2013, the pace of governance reform has accelerated. The combined reform effort in Japan has seen material improvement in corporate profit margins and return on equity since 2012. Importantly, margins and ROE remain well below those of the world index, implying significant room for improvement from here.

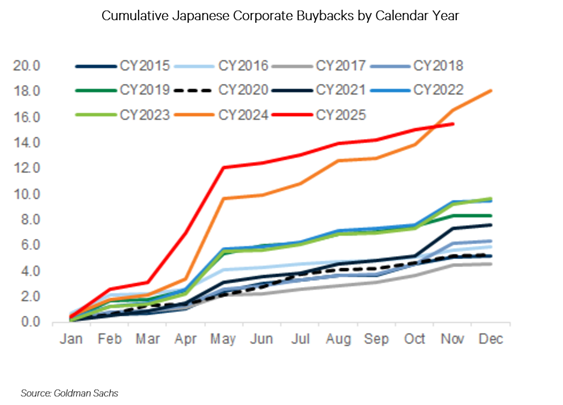

Additionally, corporate buybacks have accelerated in the past two calendar years, implying that corporates are finally beginning to see the benefits of returning excess cash to shareholders.

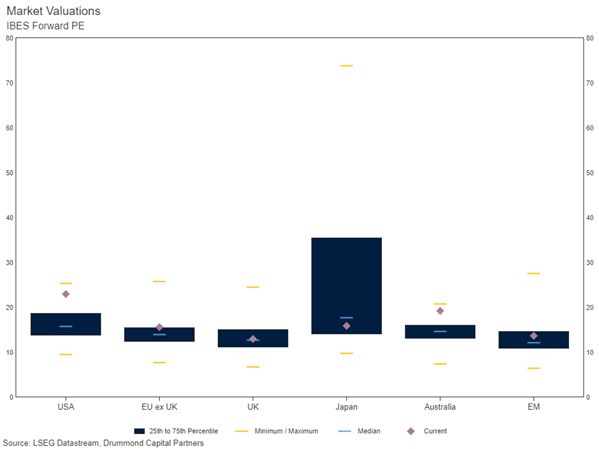

The positive reform story sits amongst a backdrop of relatively attractive valuations for the market as a whole. Japan’s forward PE is trading much lower than the US or Australia, below its historic median and around the same ratio as Europe, which lacks reform or growth prospects. Meanwhile, investors are still generally underweight Japanese equities in global equity mandates.

Portfolio Considerations

We recently added a small exposure to Japanese equities via the iShares MSCI Japan ETF. With the portfolios now overweight growth the Japan exposure has a dual objective. In an absolute sense, and inline with the above, we are positive about prospects for the country’s equity market. In addition, as the portfolios move overweight growth, we think diversifying global equity exposure away from US mega-cap technology companies is prudent. Thus, the Japan exposure sits alongside an Asia ex-Japan ETF and global small cap exposure as meaningful diversifying lines from global passive in the portfolios.

Prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only.

The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatements of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance.

This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that it is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.

-p-500.png)