.png)

Key Points:

• Despite some green shoots late last year, the Australian economy has again turned a corner for the worse, with inflation too high and the RBA again raising rates as a result.

• We think excessive government spending, lack of economic reform and too much regulation are key drivers of this outcome.

• The recently released budget does little to solve this malaise and therefore we are happy to remain underweight Australian equities in a rising interest rate and soggy growth environment.

We gave an update on the outlook for the Australian economy late last year, titled “Green Shoots in Australia.” The key theme behind that note was that with a sufficiently large RBA easing cycle, the Australian economy could potentially move out of the doldrums despite excess government spending and regulation, weak productivity growth and an over-reliance on the property market. Sadly, that has not been the case, with some improvement in our Growth Barometer late last year petering out with RBA rate hikes and Iran War. Inflation domestically has not eased sufficiently to give the RBA capacity to loosen monetary conditions. Indeed, it has gone the other way, and the RBA has raised the cash rate target three times since our note. With that in mind, and coming off the back of a recently released budget delivering meaningful changes to domestic taxation arrangements, this month we provide an update on the outlook for the Australian economy.

It is easy to blame the government for the economy’s current predicament – so we will. A lot of what has gone wrong with our economy in the past decade has been driven by poor government policy. Both sides of the aisle have contributed to our malaise, at the federal, state and local level. This failure can be summarised into three categories. Too much spending, too much regulation and too little reform.

Drunken Sailors

It is hard to argue that the material increase in the size of the government relative to the entire economy (see chart below) hasn’t had some crowding out effect on the private sector. Total government (local, state and federal) spending as a share of the economy has risen from around 23% between 1990 and 2020 to around 28.5% this year. This represents around $160 billion dollars of extra spending relative to the “norm”. To put that in perspective, that’s a similar amount to the total federal spend in 2025/26 FY on Medicare, the PBS, aged care, child care subsidies and the NDIS combined.

The impact of crowding out is hard to capture quantitatively. But the principle is intuitive. Every construction worker fortunate enough to be employed on a Tier 1 state government funded construction project (say for example building a rail line connecting middle to outer suburbs with ample road connections where a bus route would serve adequately) is a worker not available to build gas pipelines to ports, data centres or residential housing. Every excess NDIS worker is a missing childcare employee, teacher aide or aged care worker. More demand means above market wages for workers employed in related sectors and fewer workers available to be employed in productive sectors of the economy.

This week’s federal budget was a missed opportunity to resolve some of these issues at the Federal level. Some work was done on the NDIS, with proposed spending growth cuts theoretically reducing the cost of the program from an expected $110 billion per annum in 2036 to just under $80 billion. However, that’s still a material increase from the current cost ($50 billion) and many multiples of what the program was originally expected to cost when first implemented (around $30 billion per year from 2030s onwards). Additionally, whether these proposed changes will actually work, especially given the wild cost overruns of the program so far, is uncertain.

With the theoretical positive out of the way, let’s move to the negatives. Inflation is a problem in Australia. The RBA is raising rates to try and stem it. This budget, via active spending decisions, will make the problem worse. The government is proposing to increase spending, relative to its previous budget, in the next three years (see below). Beyond this, spending as a share of the economy is projected to be flat at around record levels (outside of recessions, where stimulus generally kicks in). Call us sceptical, but it’s hard to believe that no government in the next 10 years, or this government in the remainder of its term, will decide to increase their chances of re-election with a new spending commitment. Also, this projected spending path will only be this “low” if the NDIS cuts actually work. This is the time to actively cut spending. Inflation is too high. The RBA is raising interest rates. The government should be taking an axe to its budget and allow the RBA to cut rates to offset the impact.

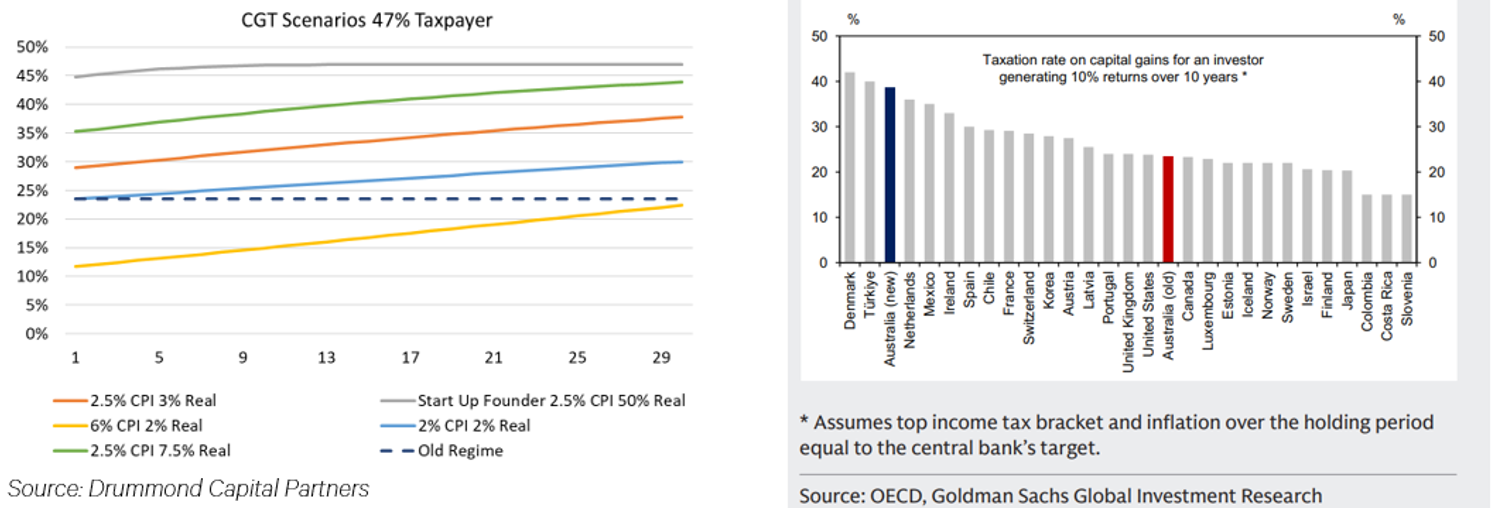

Outside the NDIS, most of the “repair” in this budget is achieved via higher taxes on investment. From 1 July 2027, the existing 50% capital gains tax discount will be replaced with an inflation-based discount and a minimum 30% rate applied to real gains. Negative gearing against wages will be limited to new builds from the same date, with existing holdings grandfathered. A minimum 30% tax on discretionary trust distributions follows from 1 July 2028. The business-side measures (reintroduced loss carry-back, loss refundability for start-ups, a permanent $20,000 instant asset write-off, expanded venture capital incentives and a recalibrated R&D tax incentive) are modest in scale relative to the investment tax changes.

The changes to CGT are problematic. There is a reason why capital gains across most economies are taxed at lower levels than income, and it’s not to make the rich richer. Applying a lower rate of tax on investment encourages saving, which deepens the capital stock and generates productivity growth, and encourages business formation. As designed, this is a tax increase on saving and risk-taking. Across most return scenarios, CGT will be higher than under the previous regime (see below). The increase is particularly punitive for business founders who, when successful, can see the value of their hard work and risk increase extremely quickly. We fear many innovators and founders will choose to leave the country and re-form or start businesses in more tax friendly regimes.

The introduction of a minimum tax of 30 per cent on discretionary trusts is fair, with the mechanism long being used to avoid tax. The negative gearing changes to property are probably a good idea. If they were expanded to existing investment property owners they would probably have a meaningful impact on existing house prices, but grandfathering should limit that effect. Regardless, this country has an unhealthy obsession with property speculation and directing marginal investment away from residential property is a good thing, even if it creates dual taxation regimes for different asset classes.

These higher taxes have been sold to the public as an attempt to improve intergenerational fairness, but they will do very little to improve the lot of the young people they were targeted at. Negative gearing changes won’t impact those who already own multiple properties, but they will capture young people trying to get ahead. Minimum capital gains tax rates above income tax rates for lower income earners will discourage saving from younger people. Intergenerational equity would be better addressed via changes to age pension asset tests, superannuation taxation arrangements, land taxes and estate taxes. The government has also done nothing to address arguably two of the largest drivers of expensive housing in the country (which is the main thing that matters for generational equality), very high rates of overseas migration (above our capacity to supply new housing) and the restriction of housing supply via heritage and other land use restrictions. While the latter is state and local council driven, the federal government could incentivise them to act if they wished. All of this is happening against a backdrop of stalled productivity.

Work Harder Not Smarter

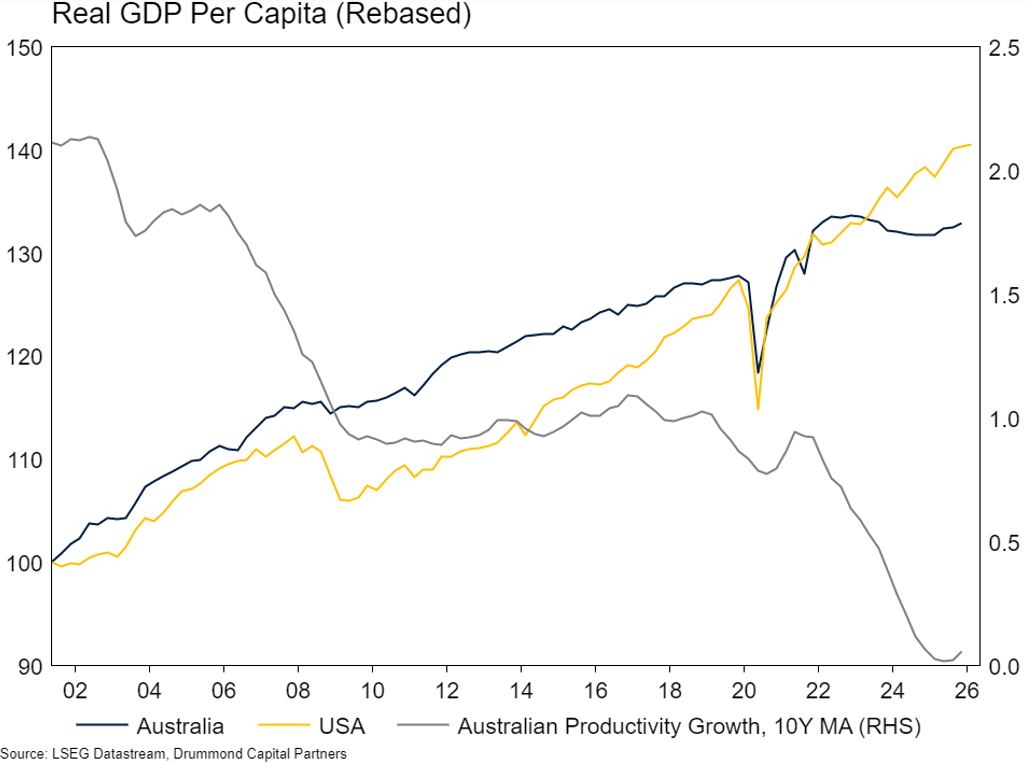

We are objectively poorer as a country than we need to be because there has been no meaningful effort from government in the past 20 years to make us richer. Real GDP per person in Australia has been stagnant since 2022 (see below), in line with no productivity growth in the economy. The budget doesn’t do much to change this. Higher capital gains taxes risk worsening our productivity problem via reduced business formation.

Over the last two decades, only a handful of reforms have actually made the economy more efficient. We count 11 reviews and enquiries, five Productivity Commission reports, and three roundtables. Each has produced detailed recommendations from credible people that for the most part have been ignored. Reform over two decades includes a half-implemented company tax cut, beefing up ACCC powers, superannuation consolidation, fewer industrial awards and the asset recycling program. Much of what governments have called "productivity reform" over this period has actually been regulation. The Fair Work Act and its successors re-regulated the labour market. The Hayne Royal Commission response built a thicket of new conduct and accountability rules across banking, insurance and superannuation and left most Australians unable to access affordable advice. The Your Future Your Super performance test forces super funds to hug benchmarks instead of building portfolios that suit members.

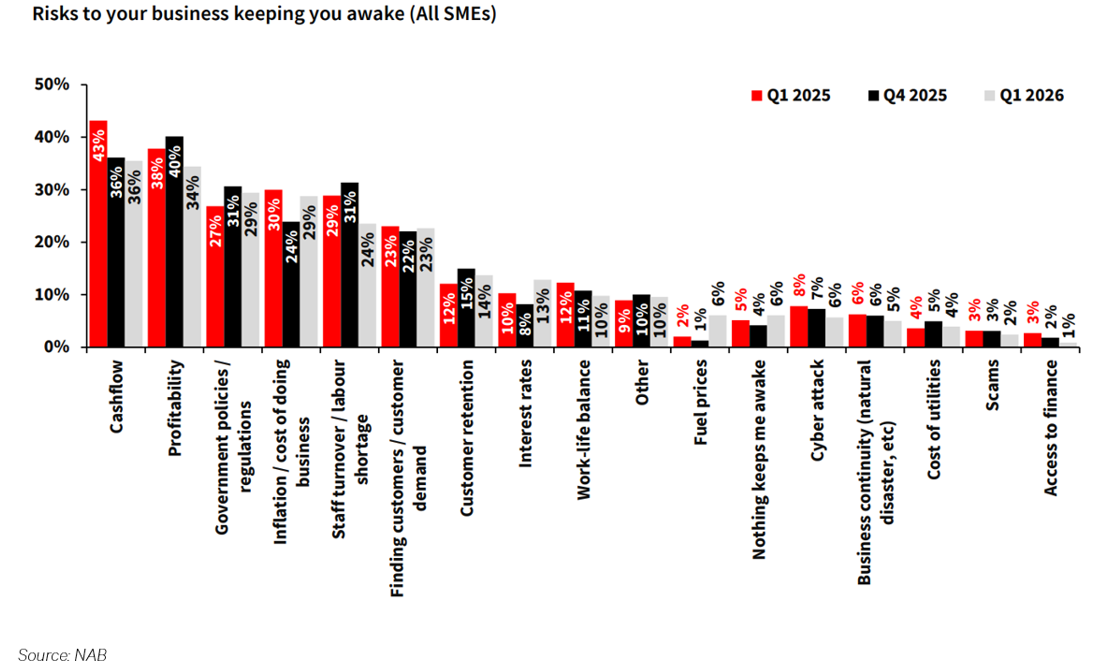

The mandatory reporting regime has exploded across every domain a business operates in. Financial-conduct reporting alone now spans the Financial Accountability Regime, ASIC breach reporting, AUSTRAC suspicious matter and threshold transaction reporting, and country-by-country tax and public tax transparency disclosures. Social and environmental disclosure has added workplace gender equality, gender pay gap, modern slavery, payment times and climate-related financial disclosures. Cyber and data obligations bring notifiable data breaches, critical infrastructure cyber incident reporting and mandatory ransomware payment reporting. SMEs are insulated from some of this, but still face a considerable burden. The NAB SME business survey below shows that government policies and regulations are third on the list of keeping owners awake at night. That’s not something the government should be proud of.

Impact on the Market

The Australian equity market, while expensive, has done a pretty lacklustre job of delivering earnings growth over the past twenty years. Earnings here have grown at a compounded rate of 1.8% per annum since mid-2006, compared with growth of 6.6% in the S&P500. Outside a resources boom, there really isn’t much we can hope for which will address this. The budget changes won’t make the economy any more dynamic. If anything, the change to capital gains tax makes it less likely that innovative companies will be founded and listed here. The Australian technology sector (which has been the key driver of earnings growth in global equity markets) is a fraction of the size of its global counterpart.

The stimulatory nature of the budget (more spending in the next few years before theoretical spending cuts via NDIS are implemented) means the RBA has more work to do on interest rates. With the government taking up an even greater share of the economy and interest rates rising, it’s hard to get excited about the economy overall. We think we are in for more years of very lacklustre growth unless something dramatic changes.

Portfolio Positioning

Our portfolios are currently neutral growth exposure, but we are underweight Australian equities. The outlook for the domestic economy is not positive, and we see little reason to be overweight our equity market.

Prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only.

The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatements of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance.

This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that it is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.

-p-500.png)