Key Points:

• Conflict in Iran continued over the weekend, driving oil futures sharply higher on Monday

• In response to geopolitical risk and higher oil prices, major equity markets continued to selloff. The Australian market is down ~5% from the peak, the US market is off around 3% and less than 1% for the year.

• If high oil prices are sustained, most models suggest around a 1% drag on global GDP growth and a 2% lift in global inflation. Not an ideal scenario, but a long way from a global recession. The global economy is much less sensitive to oil prices now than it was in previous decades.

• Futures markets expect the oil price to fall in the coming quarters, likely pricing in some combination of Trump losing interest and declaring victory, or sufficient military intervention in the Strait to make it again safe for shipping.

• We are continuing to monitor the situation and our portfolios to determine if any changes from our current positioning are appropriate.

On 28 February 2026, Israel and the United States launched a coordinated military operation against Iran, codenamed Operation Epic Fury. The strikes targeted Iran’s leadership, nuclear programme, missile sites, military facilities and regime infrastructure. On 1 March, Iranian state media confirmed that Supreme Leader Ayatollah Ali Khamenei had been killed in the strikes, along with his daughter, son-in-law, grandson, and senior IRGC commanders.

Iran responded aggressively, launching ballistic missiles and drones at US assets and allies across the region. Targets included Israel, Saudi Arabia (Riyadh and Eastern Province), the UAE (Abu Dhabi and Dubai), Bahrain (US Fifth Fleet HQ), Kuwait (Ali al-Salem air base), Qatar (Al Udeid air base), Jordan and Oman.

Mojtaba Khamenei, Ali Khamenei’s son, was named new Supreme Leader on 8 March. Iranian Foreign Minister Araghchi has rejected calls for a ceasefire, though Iranian President Masoud Pezeshkian announced that Iran will halt missile attacks on neighbouring countries unless provoked, following temporary leadership council approval. Subsequent to this announcement there have been other attacks on neighbouring countries however, calling into question who is actually controlling Iran’s armed forces at present. There has been no sign of de-escalation so far.

The only major investment implication of this conflict is on global energy markets and the flow-on effect to the economy. Iran only produces around 4% of the global oil supply, but Iranian military has effectively closed the Strait of Hormuz, through which around 20% of global oil production is transported. This, alongside attacks on nearby oil infrastructure has seen the price of oil rise to around $115 per barrel on Monday before retreating to below $90 per barrel Tuesday morning. A little below the price post Russia’s invasion of Ukraine (~$130 per barrel) and around the average of the post Financial Crisis recovery period but clearly elevated by historical standards. Unless there is a very speedy resolution to the Strait’s blockade, it seems likely the price of oil will continue to rise from here, as workarounds will take time.

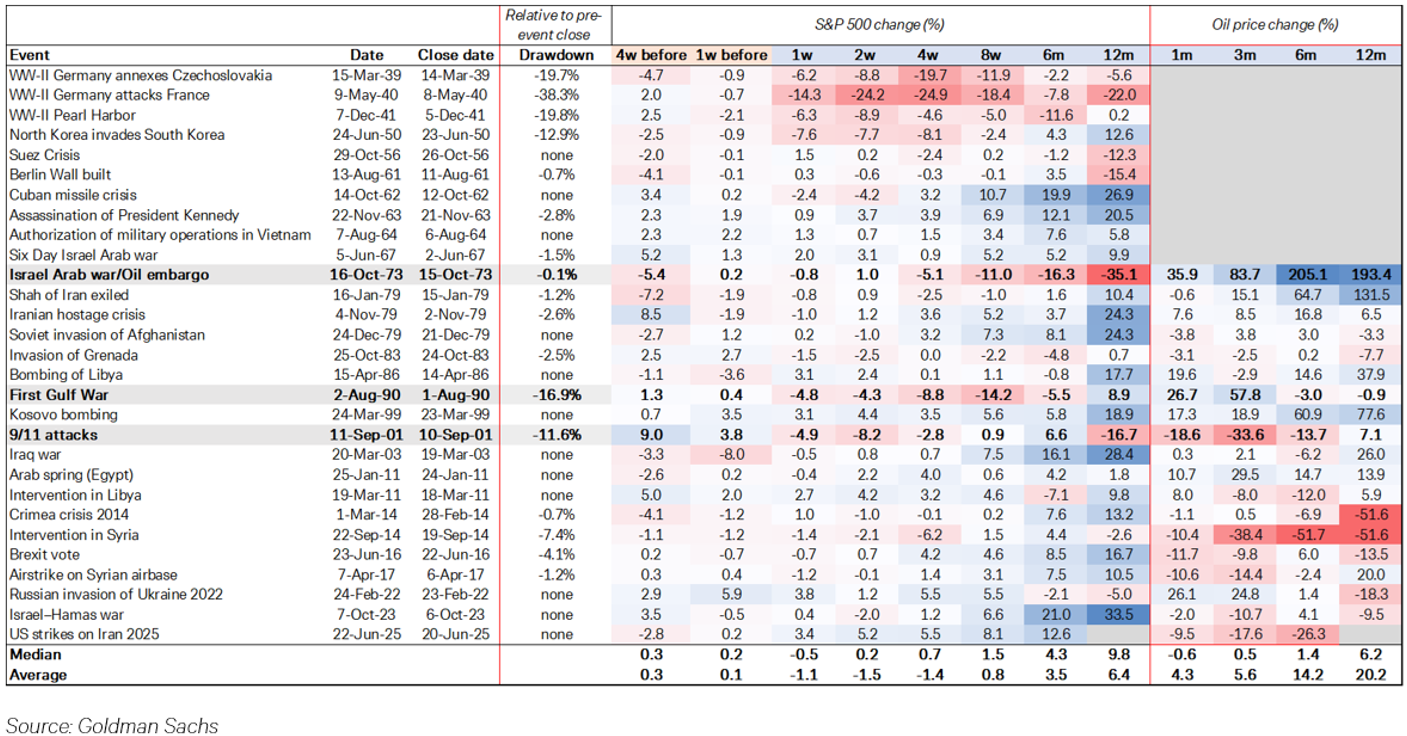

Although the primary impact is on energy markets, equities have been impacted. Major global equity markets have sold off sharply, though not materially in aggregate, with higher oil prices. The Australian market is down ~5% from the peak, the US market is off around 3% however both started 2026 strongly and have only given up year to date gains. Markets do tend to sell first and ask questions later on geopolitical events such as this and the magnitude is within the range of a normal pull back equity markets often experience. However, they also recover quickly as shown in the below table, with the median 12 month return for the S&P500 post a geopolitical event being 9.8%.

The major question for non-commodity investors is to what extent will higher oil prices be sustained and to what extent will that impact the global economy and markets. Most macroeconomic models have the impact of a sustained price shock at around a 0.1% fall in global GDP and 0.2% rise in global inflation for every 10% price increase in oil. So, all else equal and assuming sustained, the price increase we have seen so far could drag ~1% from global GDP growth and raise global inflation by around 2%. Generally, central banks will look through higher inflation generated by commodity price shocks unless they expect higher price expectations to become embedded. This is less certain post 2022 however when central banks were accused of looking through transitory inflation which ended up not being very short lived. Still, 2022 came with a legacy of massive fiscal stimulus and a booming economy and extremely tight labour markets, none of which feature today. Central banks shouldn’t hike on oil price spikes alone.

It is important to highlight that the global economy is much less sensitive to oil prices than it was in previous decades. Energy efficiency has increased across the board. The amount of oil needed to generate a dollar of GDP has fallen by around half since 1990. The share of personal consumption expenditure in the US directed towards gasoline and other energy goods has fallen from nearly 6% in 1980 to 2% today.

In addition to the above, the market doesn’t expect extremely high oil prices to be sustained. The futures curve for major oil markets has risen, but remains backwardated (lower expected prices in the future), implying the market expects a resolution. If oil settles in a year’s time at around $70-$80 per barrel, the impact on the global economy isn’t likely to be that material. This explains in large part why the price of oil can nearly double and global equity markets be off less than 10%.

There are a few reasons for this. Trump hasn’t been a bastion of consistent policy direction when things haven’t gone his way. With the Supreme Leader dead and much of Iran’s military infrastructure destroyed, Trump can declare victory and move on to the next thing that catches his attention. Almost certainly he was hoping for a Venezuela type easy regime change, which doesn’t appear particularly likely at this point. The political pressure for Trump to de-escalate will only increase in the lead-up to the November mid-term elections. High petrol prices can sway a lot of votes.

Assuming the conflict isn’t resolved, there are other measures which can be taken to make the Strait “safer.” The US has announced a $20 billion reinsurance facility via the Development Finance Corporation that would cover war-related losses on a rolling basis for vessels meeting certain criteria. There has also been talk of naval escorts to offer physical protection. Realistically, the former is of fairly limited benefit, or at the very least hasn’t convinced shipping companies to resume traversing the Strait. The second point is of more relevance. Oil needs to flow, there is no short-term re-routing option for 20% of the world’s supply.

Rather than accept a closed Strait, we expect ongoing military again aiming to eradicate Iran’s navy and air force, destroy its long-distance missile launch capability and deny drone access. There is a significant amount of US (and, presumably an increasing number of allies if oil stays above $100 per barrel) military might which can be thrown into the Persian Gulf, Gulf of Oman and 34km wide Strait of Hormuz to make it safe for shipping.

Portfolio Positioning

Our portfolios are currently overweight global equities, though our equity mix is very diversified, with exposures across Asia and small caps balancing a large position in the index. Typically, geopolitical events do not trigger meaningful and protracted market selloffs and up until this point, economic growth has been accelerating supporting global earnings and equity markets. That said, we don’t want to dismiss the risk that this conflict leads to material oil supply disruptions and some slowdown in global economic growth as a result. However, based on modelling from central banks, the IMF and others, it is hard to translate the spike in oil prices into a forecast of global recession, which would generally be the catalyst needed to drive global earnings growth negative enough to lead to a market fall beyond a typical correction. There are heightened regional sensitivities in energy importing economies, but generally developed market economies are much less sensitive to energy prices than they used to be. Regardless, we are continuing to monitor the situation and our portfolios to determine if any changes from our current positioning are appropriate. Should the conflict broaden materially (China and Russia are both Iran friendly governments), or evidence emerge of a sustained global growth deterioration, we would look to reduce risk in portfolios.

Prepared by Drummond Capital Partners (Drummond) ABN 15 622 660 182, AFSL 534213. It is exclusively for use for Drummond clients and should not be relied on for any other person. Any advice or information contained in this report is limited to General Advice for Wholesale clients only.

The information, opinions, estimates and forecasts contained are current at the time of this document and are subject to change without prior notification. This information is not considered a recommendation to purchase, sell or hold any financial product. The information in this document does not take account of your objectives, financial situation or needs. Before acting on this information recipients should consider whether it is appropriate to their situation. We recommend obtaining personal financial, legal and taxation advice before making any financial investment decision. To the extent permitted by law, Drummond does not accept responsibility for errors or misstatements of any nature, irrespective of how these may arise, nor will it be liable for any loss or damage suffered as a result of any reliance on the information included in this document. Past performance is not a reliable indicator of future performance.

This report is based on information obtained from sources believed to be reliable, we do not make any representation or warranty that it is accurate, complete or up to date. Any opinions contained herein are reasonably held at the time of completion and are subject to change without notice.

-p-500.png)